Bush Signs Housing Bill

President Bush enacts controversial measure that aims to help borrowers, bolster the housing market and provide a fail-safe for Fannie and Freddie.

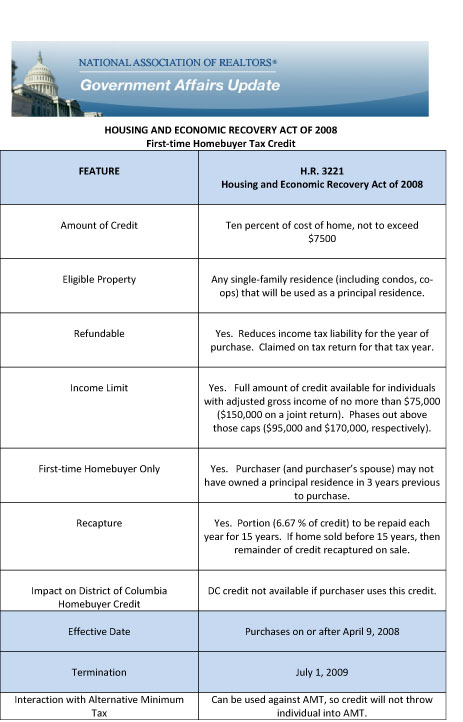

H.R. 3221, the Housing and Economic Recovery Act of 2008 — which was passed by the Congress on July 26 and signed by President Bush on July 30 — allows first-time home buyers to take a $7,500 tax credit from the purchase of a single-family home, townhome or condominium apartment.

The Senate voted 72-13 in favor of the bill on Saturday, after the House passed it three days earlier.

The legislation has two principal objectives: to offer affordable government-backed mortgages to homeowners at risk of foreclosure, and to bolster Fannie and Freddie with a temporary rescue plan and a new, more stringent regulator.

The cost of the program – which would begin on Oct. 1 and be in place for just a few years – will be funded by fees from Fannie and Freddie, along with fees paid by both lenders and borrowers.

· The law authorizes FHA to insure up to $300 billion in loans.

· A permanent increase in “conforming loan” limits. The law will permanently increase the cap on the size of mortgages guaranteed by Fannie and Freddie to a maximum of $625,500 from $417,000.

The FHA maximum loan limits for high-cost areas would also increase to a maximum of $625,500. Higher loan limits will make it easier for borrowers to get mortgages, because those mortgages are more likely to be traded if they are considered conforming.

· A new home-buyer credit. The new law includes a tax refund for first-time home buyers worth up to 10% of a home’s purchase price but no more than $7,500.00.

· A new affordable housing trust fund. The law establishes a permanent fund to promote affordable housing. The fund will be paid for by fees from Fannie and Freddie.

· Grants to states to buy foreclosed properties The law grants $4 billion to states to buy up and rehabilitate foreclosed properties.

· Fannie and Freddie guarantee the purchase and trade of mortgages and own or back to $5.2 trillion in mortgages.

Any home buyer who has not owned a home during the past three years and is a U.S. citizen who files taxes is eligible to participate in this program. (Some home buyers who are not citizens may also qualify.)

To qualify, buyers must actually close on the sale of the home on or after April 9, 2008 and before July 1, 2009. The original eligibility period expired in April 2009, but following a major grassroots campaign from NAHB members, the period was extended to enable home builders to include the credit in their sales and marketing next spring and into the early summer — the peak home buying season.

The program does have income limits. Single or head-of-household filers can claim the full $7,500 credit if their adjusted gross income (AGI) is less than $75,000. For married couples filing a joint return, the income limit doubles to $150,000.

Single or head-of-household taxpayers who earn between $75,000 and $95,000 are eligible to receive a partial first-time home buyer tax credit. The same applies to married couples who earn between $150,000 and $170,000.

The credit is not available for single taxpayers whose AGI is greater than $95,000 and married couples with an AGI exceeding $170,000.

A refundable credit means that if a taxpayer pays less than $7,500 in federal income taxes, the government will write them a check for the difference. For example, if $5,000 in federal taxes is owed, the taxpayer would pay nothing and a $2,500 payment would be received from the IRS. If a qualifying home buyer were owed a $1,000 tax refund, they would receive $8,500.

Buyers can take the tax credit on their 2008 or 2009 tax return. Those who close in 2008 take the credit on their 2008 return. Buyers in 2009 have the option of taking the credit on their 2008 or 2009 returns.

The tax-credit program also has payback provisions.

The credit essentially serves as an interest-free loan to be repaid over 15 years. For example, a home buyer claiming a $7,500 credit would repay the credit at $500 per year. If the home owner sold the home, then the remaining credit would be due from the profit of the home sale.

If there is insufficient profit, then the remaining credit payback would be forgiven.

For more information on NAHB tax credit resources, e-mail NAHB Public Affairs or call 800-368-5242 x8061.

Questions and Answers for Consumers

Following are the “Frequently Asked Questions About the First-Time Home Buyer Tax Credit” that appear on NAHB’s consumer Web site — www.federalhousingtaxcredit.com.

1. Who is eligible to claim the $7,500 tax credit?

First time-home buyers purchasing any kind of home — new or resale — are eligible for the tax credit.

2. What is the definition of a first-time home buyer?

The law defines "first-time home buyer" as a buyer who has not owned a principal residence during the three-year period prior to the purchase. For married taxpayers, the law tests the homeownership history of both the home buyer and his or her spouse. For example, if you have not owned a home in the past three years but your spouse has owned one, neither you nor your spouse qualifies for the first-time home buyer tax credit.

3. What types of homes will qualify for the tax credit?

Any home purchased by an eligible first-time home buyer will qualify for the credit, provided that the home will be used as a principal residence and the buyer has not owned a home in the previous three years. This includes single-family detached homes, attached homes like townhouses, and condominiums.

4. Are there income limits to determine who is eligible to take the tax credit?

Yes. Home buyers who file their taxes as single or head-of-household taxpayers can claim the credit if their modified adjusted gross income (MAGI) is less than $75,000. For married taxpayers filing a joint tax return, the MAGI limit is $150,000. The limit is based on the buyer’s modified adjusted gross income for the year that the house is purchased, except for certain purchases in 2009.

5. What is “modified adjusted gross income”?

Modified adjusted gross income, or MAGI, is defined by the IRS. To find it, a taxpayer must first determine “adjusted gross income,” or AGI, which is total income for a year minus certain deductions (known as “adjustments” or “above-the-line deductions”), but before itemized deductions from Schedule A or personal exemptions are subtracted. On Forms 1040 and 1040A, AGI is the last number on page 1 and first number on page 2 of the form. For Form 1040-EZ, AGI appears on line 4 (as of 2007). Note that AGI includes all forms of income — including wages, salaries, interest income, dividends and capital gains.

To determine modified adjusted gross income (MAGI), add to AGI certain amounts such as foreign income, foreign-housing deductions, student-loan deductions, IRA-contribution deductions and deductions for higher-education costs.

6. If my modified adjusted gross income (MAGI) is above the limit, do I qualify for any tax credit?

Possibly. It depends on your income. Partial credits of less than $7,500 are available for some taxpayers whose MAGI exceeds the phaseout limits. The credit becomes totally unavailable for individual taxpayers with a modified adjusted gross income of more than $95,000 and for married taxpayers filing joint returns with an AGI of more than $170,000.

7. Can you give me an example of how the partial tax credit is determined?

Just as an example, assume that a married couple has a modified adjusted gross income of $160,000. The applicable phaseout to qualify for the tax credit is $150,000, and the couple is $10,000 over this amount. Dividing $10,000 by $20,000 yields 0.5. When you subtract 0.5 from 1.0, the result is 0.5. To determine the amount of the partial first-time home buyer tax credit that is available to this couple, multiply $7,500 by 0.5. The result is $3,750.

Here’s another example: assume that an individual home buyer has a modified adjusted gross income of $88,000. The buyer’s income exceeds $75,000 by $13,000. Dividing $13,000 by $20,000 yields 0.65. When you subtract 0.65 from 1.0, the result is 0.35. Multiplying $7,500 by 0.35 shows that the buyer is eligible for a partial tax credit of $2,625.

Please remember that these examples are intended to provide a general idea of how the tax credit might be applied in different circumstances. You should always consult your tax advisor for information relating to your specific circumstances.

8. Does the credit amount differ based on tax filing status?

No. The credit is in general equal to $7,500 for a qualified home purchase, whether the home buyer files taxes as a single or married taxpayer. However, if a household files its taxes as “married filing separately” (in effect, filing two returns), then the credit of $7,500 is claimed as a $3,750 credit on each of the two returns.

9. Are there any circumstances under which buyers whose incomes are at or below the $75,000 limit for singles or the $150,000 limit for married taxpayers might not be able to claim the full $7,500 tax credit?

In general, the tax credit is equal to 10% of the qualified home purchase price, but the credit amount is capped or limited at $7,500. For most first-time home buyers, this means the credit will equal $7,500. For home buyers purchasing a home priced less than $75,000, the credit will equal 10% of the purchase price.

10. I heard that the tax credit is refundable. What does that mean?

The fact that the credit is refundable means that the home buyer credit can be claimed even if the taxpayer has little or no federal income tax liability to offset. Typically this involves the government sending the taxpayer a check for a portion or even all of the amount of the refundable tax credit.

For example, if a qualified home buyer expected federal income tax liability of $5,000 and had tax withholding of $4,000 for the year, then without the tax credit the taxpayer would owe the IRS $1,000 on April 15. Suppose now that taxpayer qualified for the $7,500 home buyer tax credit. As a result, the taxpayer would receive a check for $6,500 ($7,500 minus the $1,000 owed).

11. What is the difference between a tax credit and a tax deduction?

A tax credit is a dollar-for-dollar reduction in what the taxpayer owes. That means that a taxpayer who owes $7,500 in income taxes and who receives a $7,500 tax credit would owe nothing to the IRS.

A tax deduction is subtracted from the amount of income that is taxed. Using the same example, assume the taxpayer is in the 15% tax bracket and owes $7,500 in income taxes. If the taxpayer receives a $7,500 deduction, the taxpayer’s tax liability would be reduced by $1,125 (15% of $7,500), or lowered from $7,500 to $6,375.

12. Can I claim the tax credit if I finance the purchase of my home under a mortgage revenue bond (MRB) program?

No. The tax credit cannot be combined with the MRB home buyer program.

13. I live in the District of Columbia. Can I claim both the D.C. first-time home buyer credit and this new credit?

No. You can claim only one.

14. I am not a U.S. citizen. Can I claim the tax credit?

Maybe. Anyone who is not a nonresident alien (as defined by the IRS), who has not owned a principal residence in the previous three years and who meets the income limits test may claim the tax credit for a qualified home purchase. The IRS provides a definition of “nonresident alien” in IRS Publication 519 (www.irs.gov/pub/irs-pdf/p519.pdf).

15. Does the credit have to be paid back to the government? If so, what are the payback provisions?

Yes, the tax credit must be repaid. Home buyers will be required to repay the credit to the government, without interest, over 15 years or when they sell the house, if there is sufficient capital gain from the sale. For example, a home buyer claiming a $7,500 credit would repay the credit at $500 per year. The home owner does not have to begin making repayments on the credit until two years after the credit is claimed. So if the tax credit is claimed on the 2008 tax return, a $500 payment is not due until the 2010 tax return is filed. If the home owner sold the home, then the remaining credit amount would be due from the profit on the home sale. If there was insufficient profit, then the remaining credit payback would be forgiven.

16. Why must the money be repaid?

The intent of Congress was to provide as large a financial resource as possible for home buyers in the year that they purchase a home. In addition to helping first-time home buyers, this will maximize the stimulus for the housing market and the economy, will help stabilize home prices and will increase home sales. The repayment requirement reduces the impact on the U.S. Treasury and assumes that home buyers will benefit from stabilized and, eventually, rising future housing prices.

17. Because the money must be repaid, isn’t the first-time home buyer program really a zero-interest loan rather than a traditional tax credit?

Yes. Because the tax credit must be repaid, it operates like a zero-interest loan. Assuming an interest rate of 7%, that means the home owner saves up to $4,200 in interest payments over the 15-year repayment period. Compared to $7,500 financed through a 30-year mortgage with a 7% interest rate, the home buyer tax credit saves home buyers more than $8,100 in interest payments. The program is called a tax credit because it operates through the tax code and is administered by the IRS. Also like a tax credit, it provides a reduction in tax liability in the year it is claimed.

18. If I’m qualified for the tax credit and buy a home in 2009, can I apply the tax credit against my 2008 tax return?

Yes. The law allows taxpayers to choose (“elect”) to treat qualified home purchases in 2009 as if the purchase occurred on Dec. 31, 2008. This means that the 2008 income limit (MAGI) applies and the election accelerates when the credit can be claimed (tax filing for 2008 returns instead of for 2009 returns). A benefit of this election is that a home buyer in 2009 will know their 2008 MAGI with certainty, thereby helping the buyer know whether the income limit will reduce their credit amount.

19. For a home purchase in 2009, can I choose whether to treat the purchase as occurring in 2008 or 2009, depending on in which year my credit amount is the largest?

Yes. If the applicable income phaseout would reduce your home buyer tax credit amount in 2009 and a larger credit would be available using the 2008 MAGI amounts, then you can choose the year that yields the largest credit amount.

Source: CNN Money, Federal Housing Tax Credit

![]()

posted by Will @ 2:44 PM

0 comments

![]()

![]()