Convenience and location make Jacksonville's Southside a popular place to live. Centrally located, the Southside is bordered by Arlington to the north and east, St. Johns County to the south and San Marco and I-95 to the west. This is literally the southernmost area of urban Jacksonville and is in the middle of all other Jacksonville communities. Surrounded by San Jose, Arlington, Mandarin and the Beaches, Southside has the area's largest grouping of apartment communities. Many new developments are less than a year old. Many Jacksonville residents may think of the Southside as predominantly new development. This perception is understandable. Growth in the area over the last two decades has been rapid and well publicized. Neighborhoods range from working class, single-family homes, condominiums and townhomes to upscale gated and golf communities with many amenities. The area is home to a mix of architectural styles such as bungalow, contemporary, Western ranch, Tudor, traditional, farmhouse, Cape Cod, Colonial, French country, Mediterranean, Spanish, Victorian and brownstone. The city maintains an extensive network of parks all over the Southside including neighborhood, preservation, and community parks. Various parks offer a mix of playgrounds, swimming pools, trails, picnic and cooking areas, sports and multi-use fields, lighted tennis courts, concession areas and community centers. Commuting, shopping and recreation are convenient. Residents enjoy local golf courses, abundant dining and entertainment, grand shopping centers like Tinseltown and St. Johns Town Center, and easy access to the beaches via J. Turner Butler Boulevard.

Search Jacksonville MLS listing, homes for sale, condos for sale, rental homes, vacant land, commercial and residential real estate.

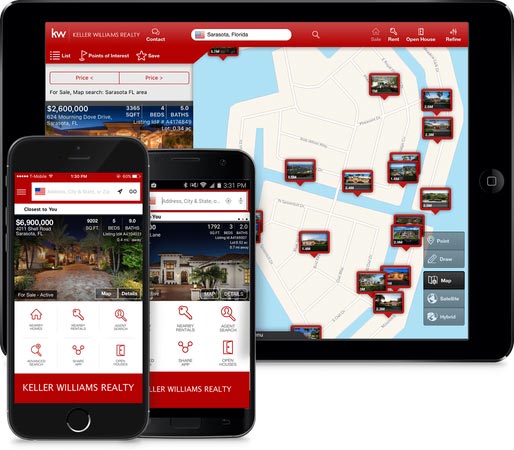

Download the KW Mobile App

Are you looking for a new home? Curious about what's for sale in your neighborhood? Want to find open houses nearby? The Keller Williams mobile app allows you free access to more than 4 million homes on the market.